Personal Loan Underwriting with Cashflow Analytics

Predict the likelihood of personal loan payments to reduce defaults. Drive lift in your risk models for personal loans with Cashflow Attributes and Scores.

Enhance Personal Loan Underwriting with Predictive Cashflow Scores

Enhance risk models for personal loans with the Personal Loan Score and Cashflow Attributes.

Improve Risk Models for Personal Loan Underwriting

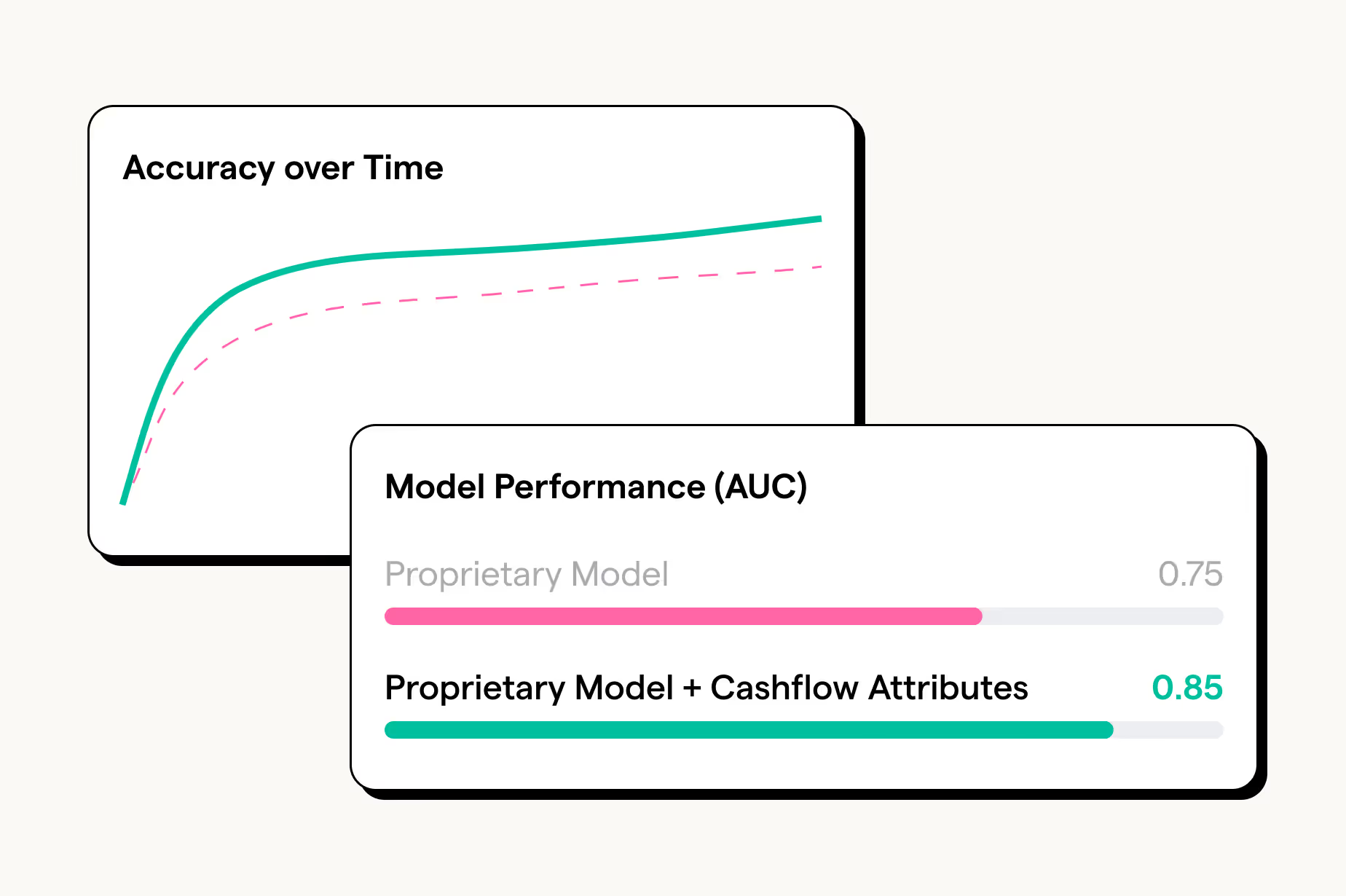

Enhance proprietary models with Cashflow-driven Attributes and Scores to more accurately assess borrower affordability, identify healthy borrowers, and unlock new segments.

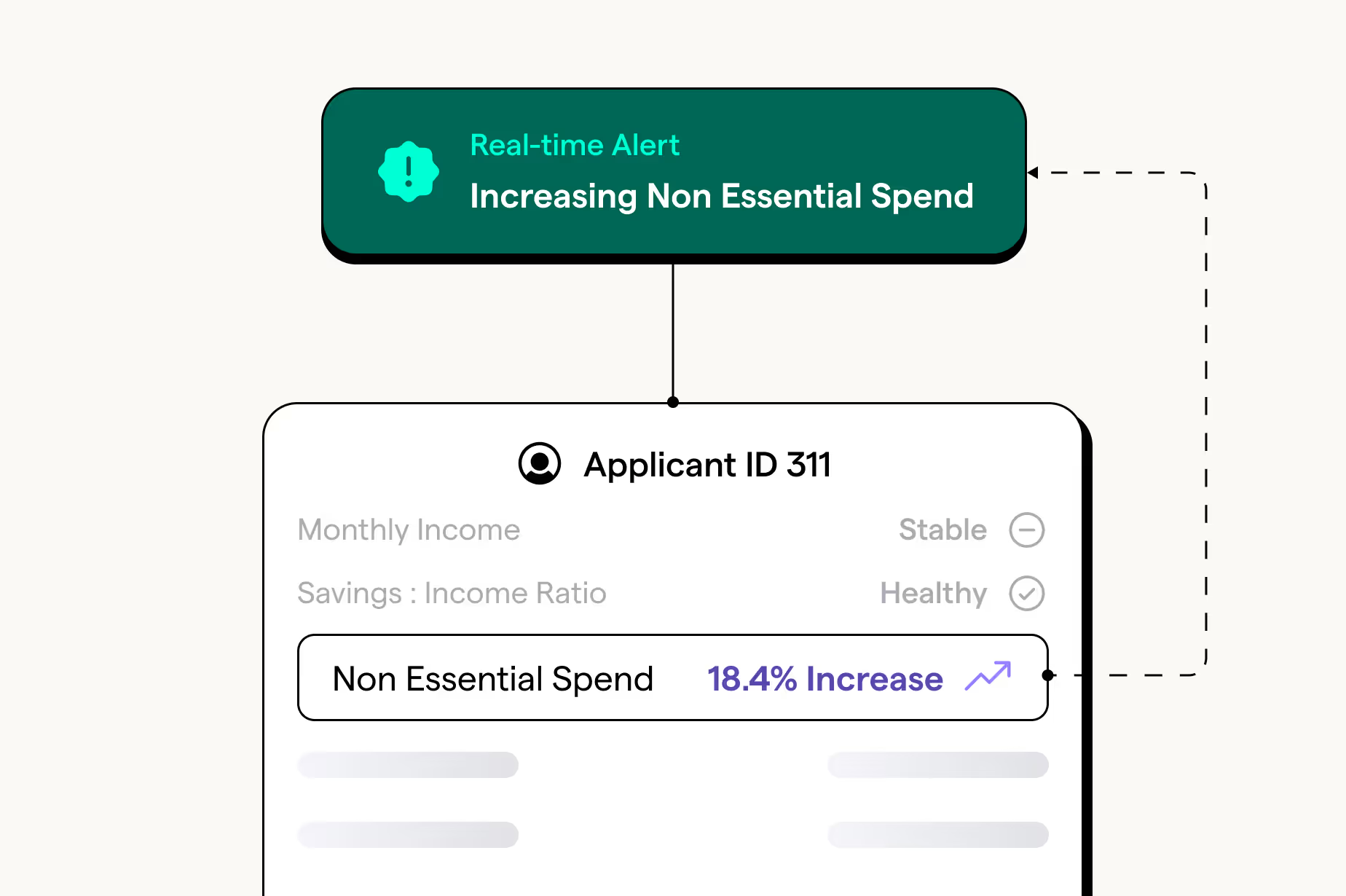

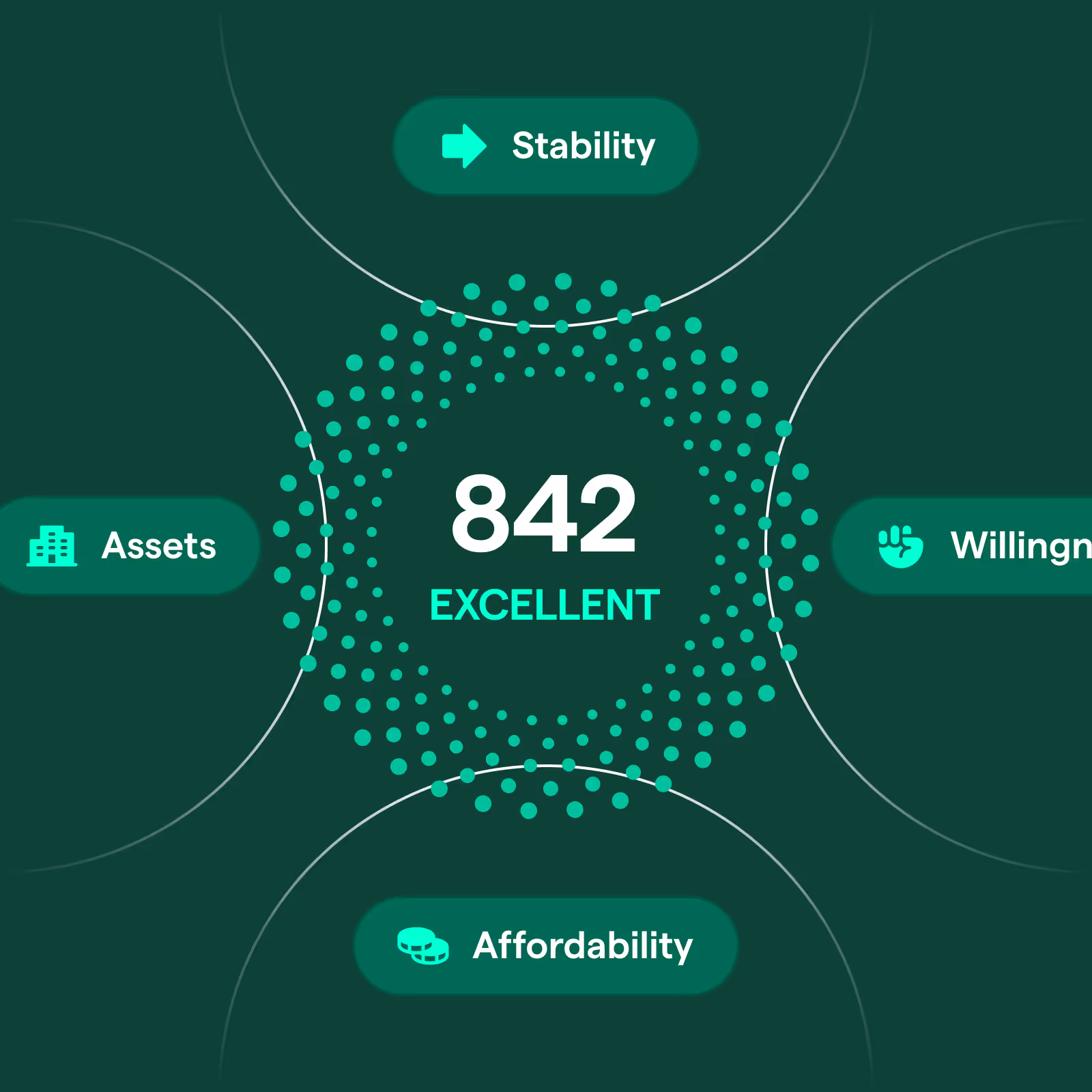

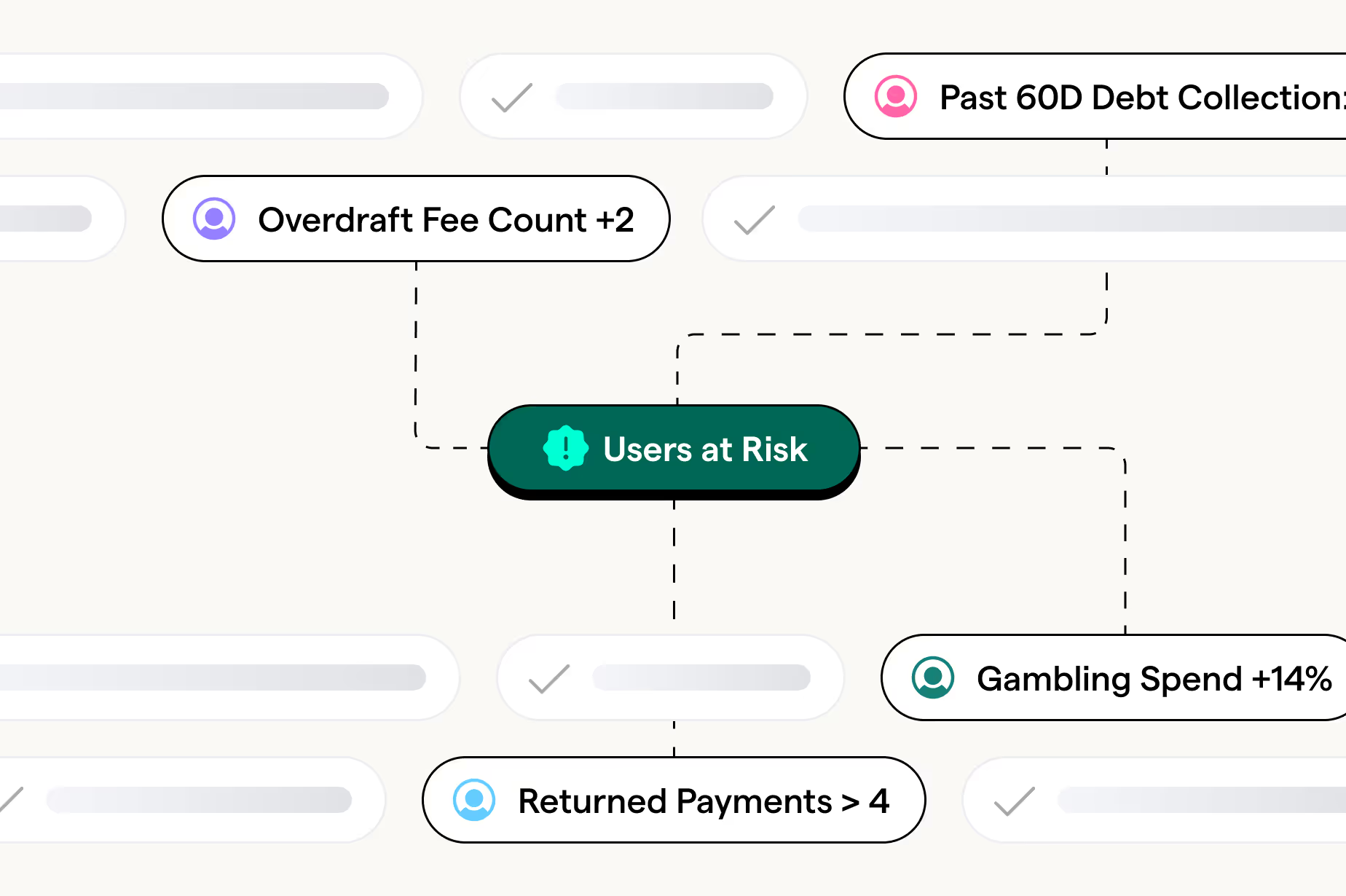

Monitor Borrower Cashflow in Real Time

Track real-time income stability, spending, and financial health to adjust loan amounts, foster growth, and proactively mitigate risks before they impact your portfolio.

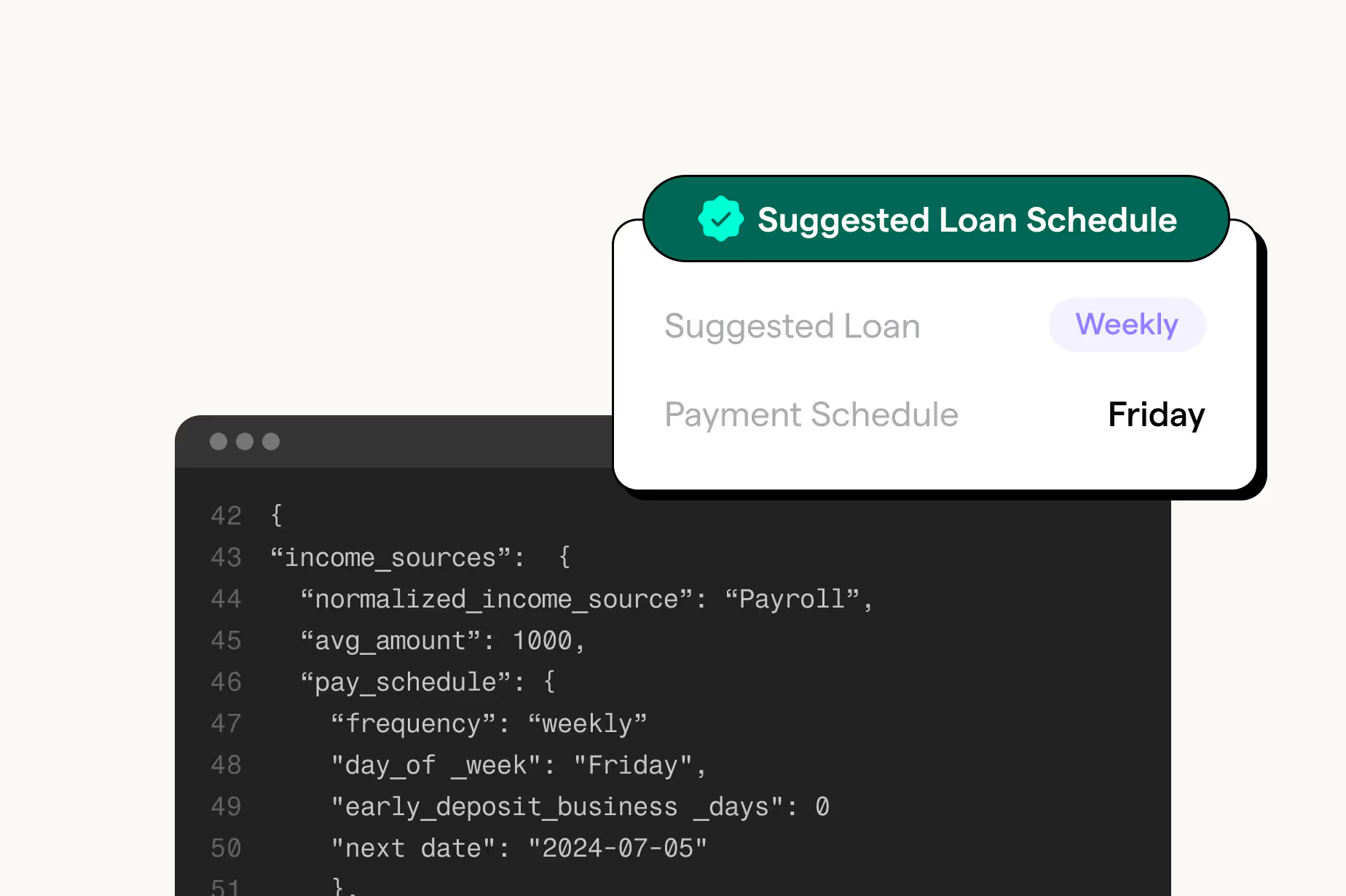

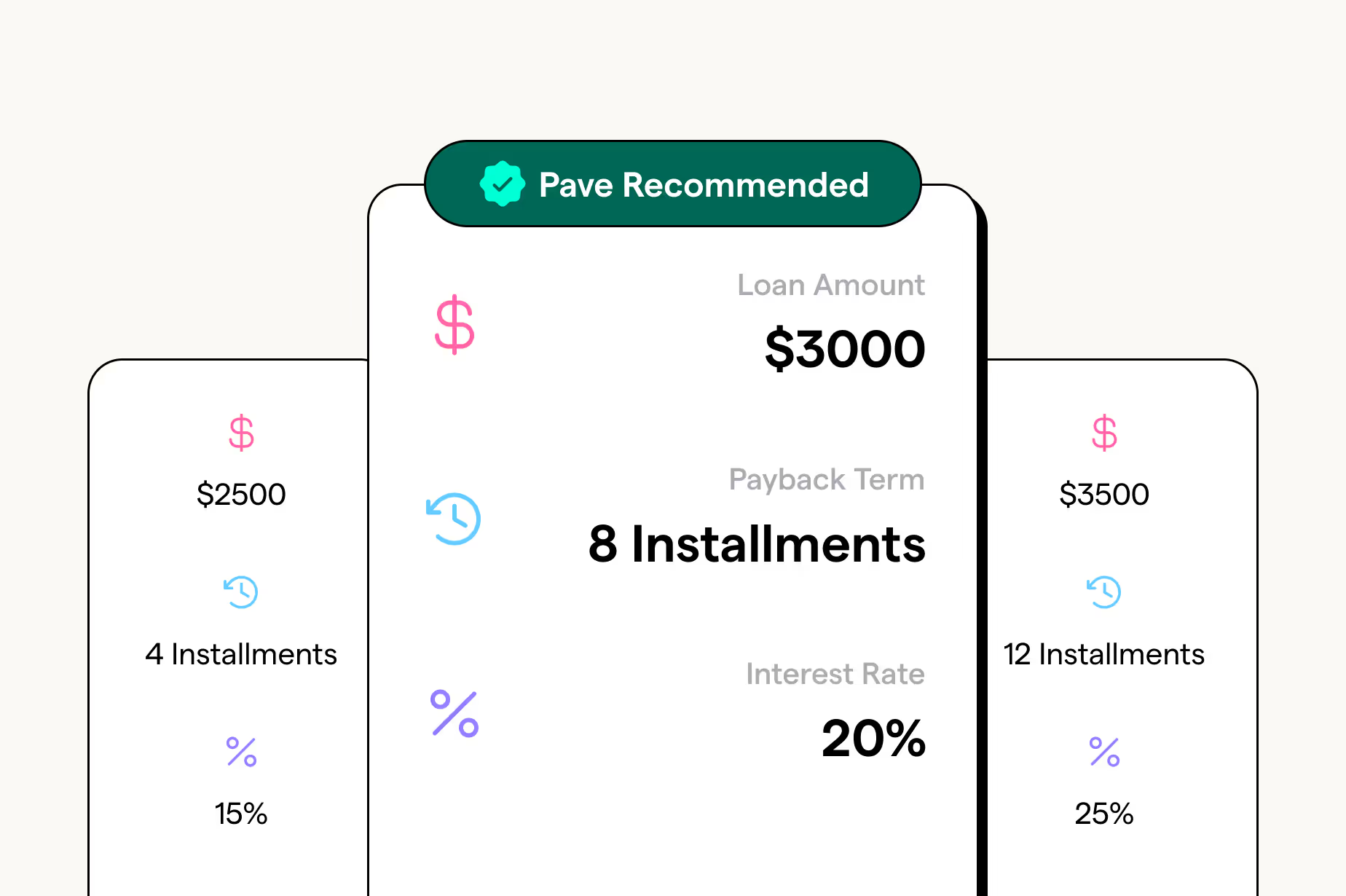

Personalize Personal Loan Repayment Plans

Align payment schedules with borrowers' income to improve on time payments and reduce risk.

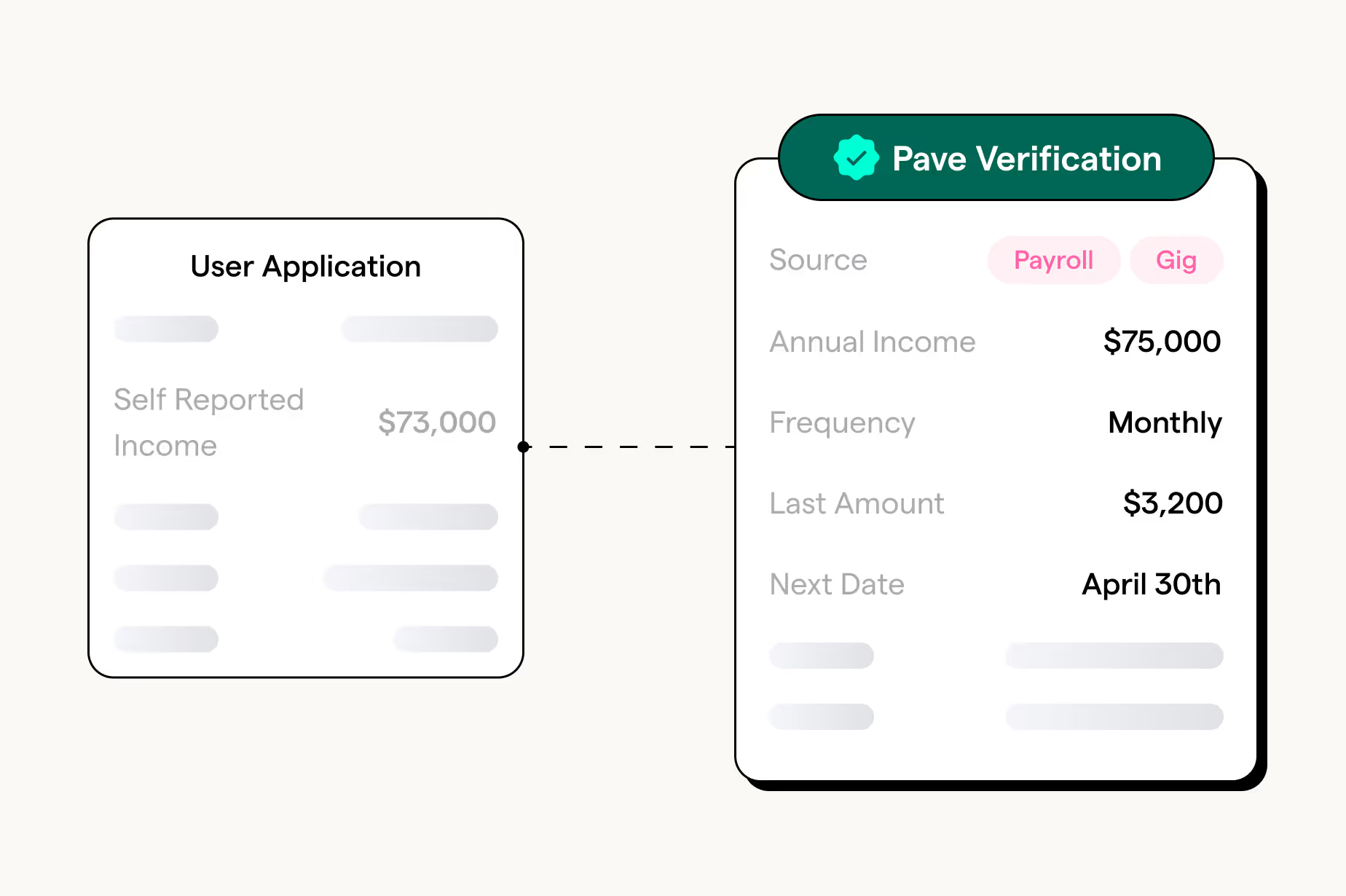

How Cashflow Data Improves Personal Loan Underwriting

Cashflow analytics provides lenders with deeper insight into borrower affordability, income stability, and spending behavior. By integrating real-time transaction data into underwriting models, lenders can more accurately predict repayment likelihood and expand access to responsible personal loans.

FAQ

How does cashflow data improve personal loan underwriting?

Cashflow analytics provides real-time insight into borrower income, expenses, and financial stability, enabling lenders to better assess repayment capacity.

What data is used in personal loan underwriting models?

Underwriting models can use bank transaction data, income patterns, liabilities, and spending behavior to evaluate borrower affordability.

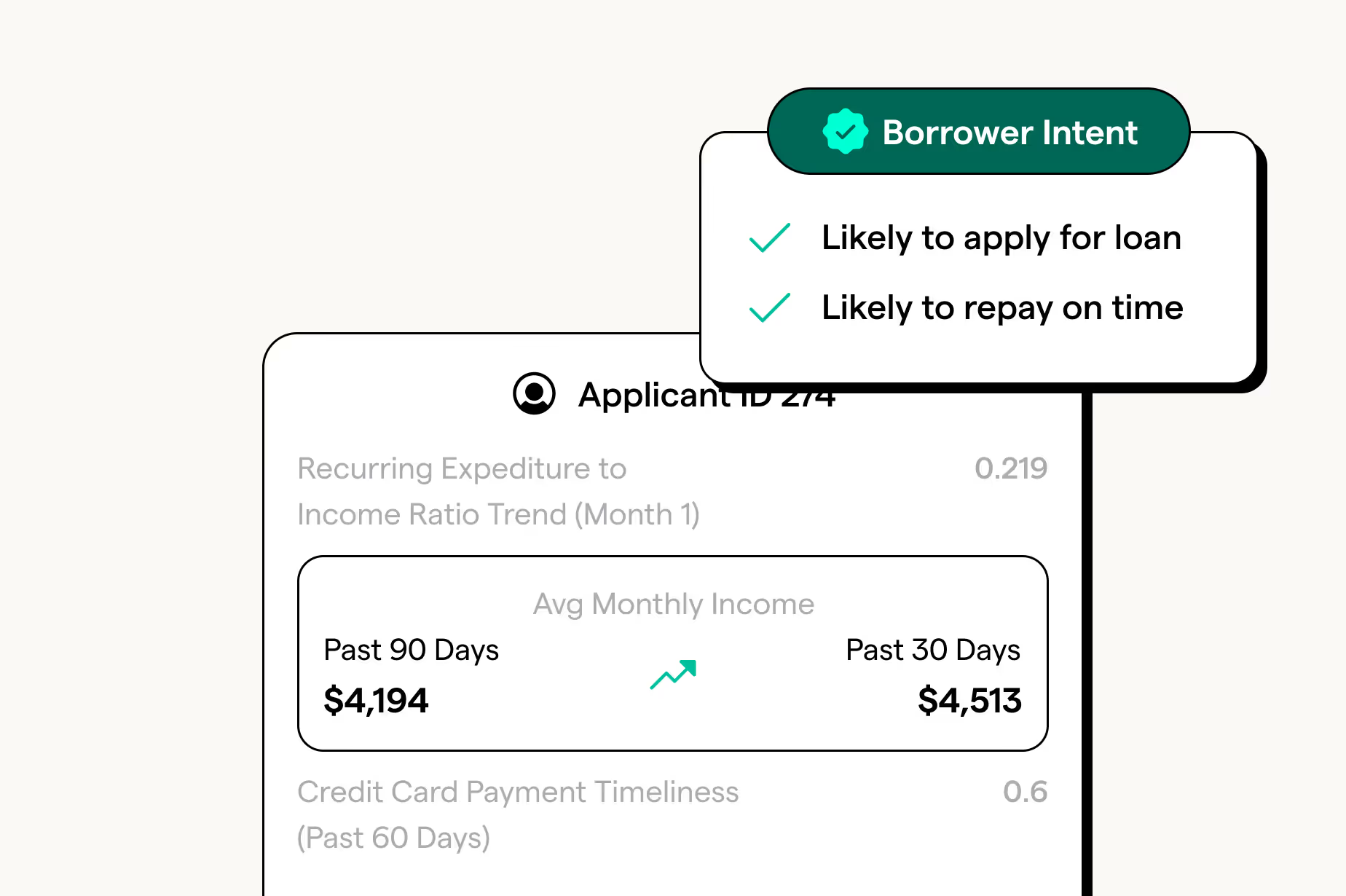

Can cashflow analytics reduce personal loan defaults?

Yes. Cashflow-based scoring models help lenders identify financially stable borrowers and detect risk signals earlier.

Explore More Products

Cashflow Scores

Offer higher amounts and drive growth with our Cashflow Scores, built on Cashflow Attributes and repayment history. Increase approvals and retention by identifying healthy, underserved borrowers.

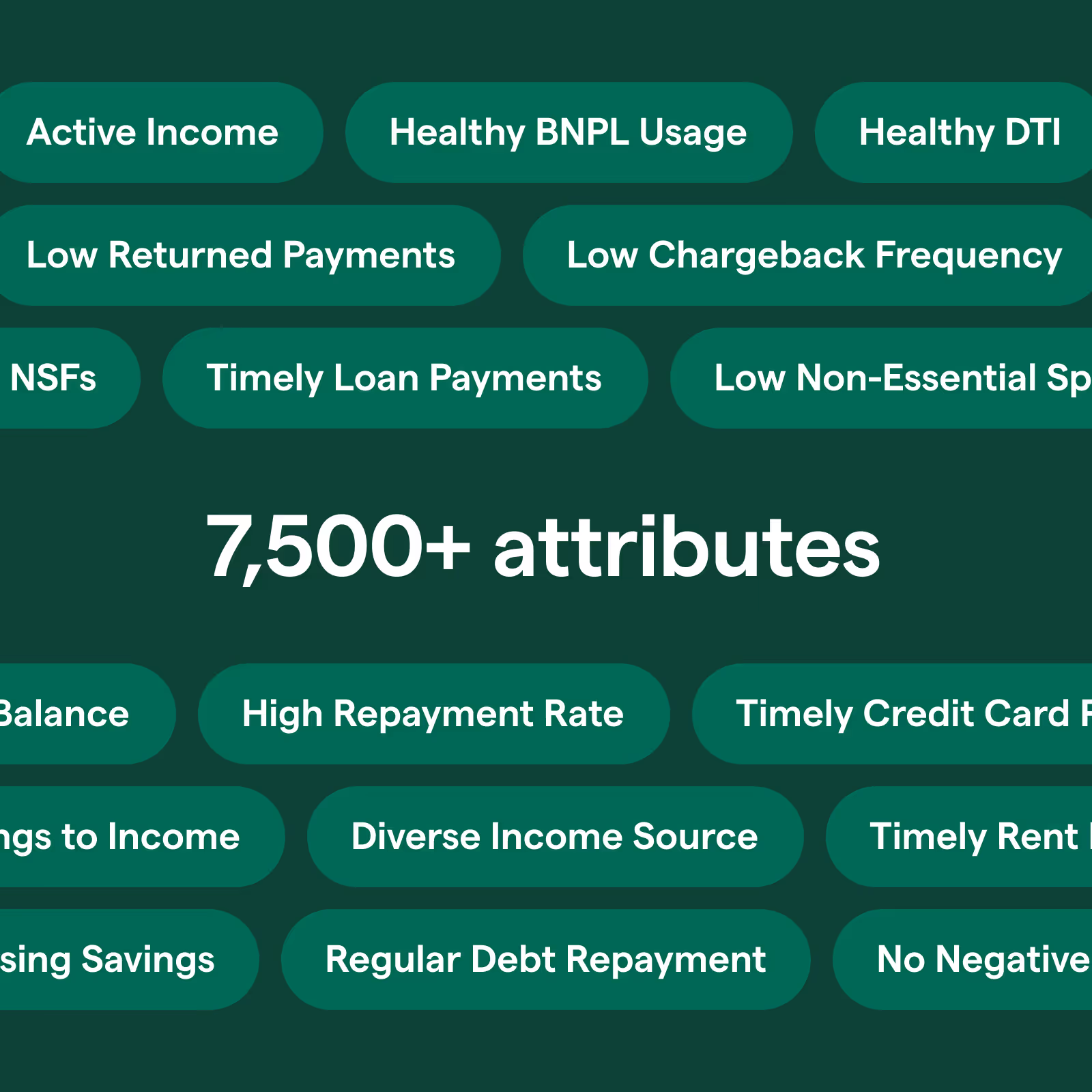

Cashflow Attributes

Drive lift in your risk models to boost approvals with thousands of pre-built attributes built on our expansive loan performance dataset.

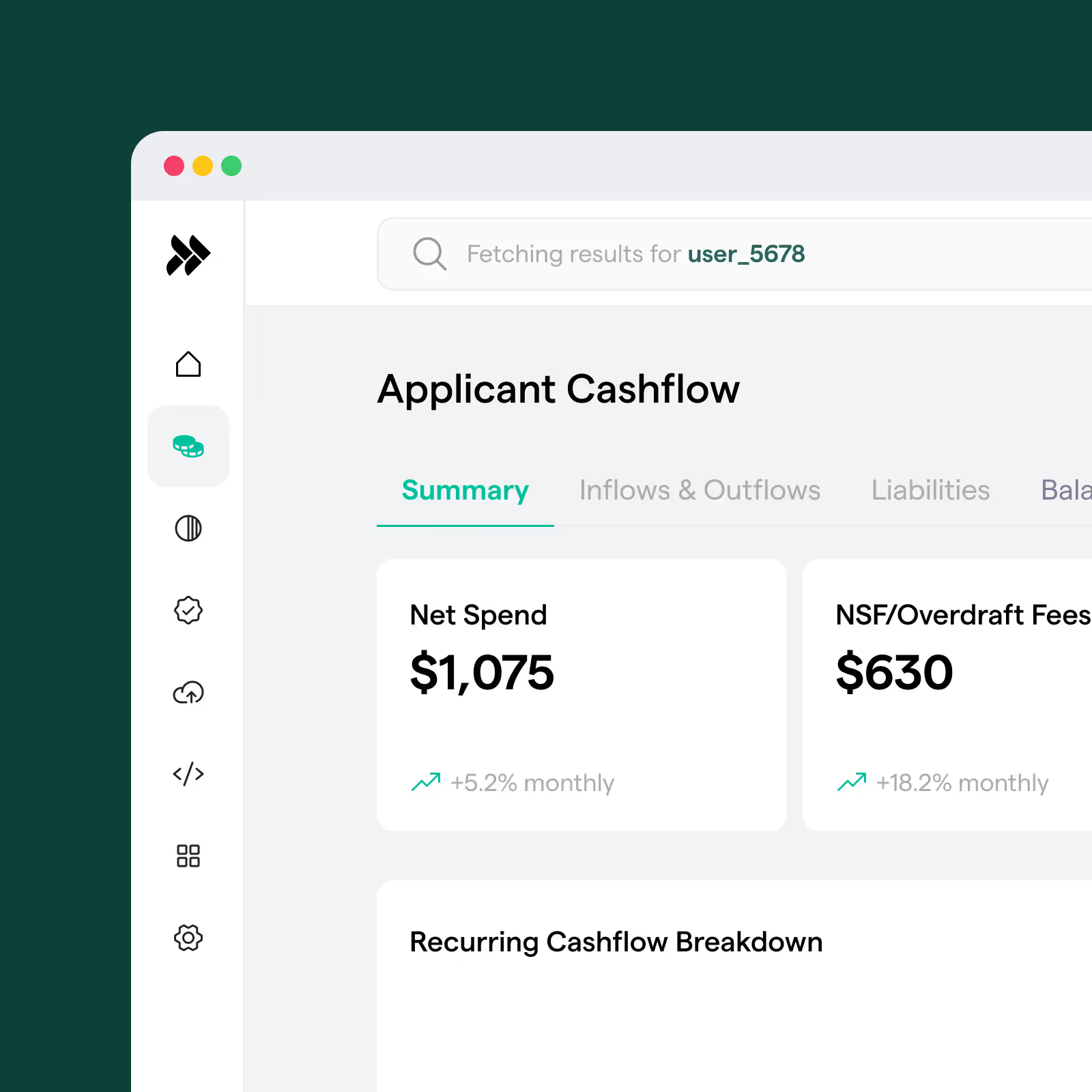

Cashflow Analytics

Automate processes to increase approvals and serve more borrowers using Pave’s real-time Cashflow Analytics. Streamline operations and identify healthy, underserved borrowers.

Cashflow Analytics in Snowflake

Gain seamless access to cashflow data within Snowflake to enhance analysis and decision-making. Leverage Pave’s standardized tables, updated daily, to uncover insights without complex ETL.

Related Posts

Drive growth with Cashflow-driven Analytics

Use our Cashflow-driven Attributes and Scores to provide timely, borrower-specific insights tailored to your lending criteria. Make informed decisions that enhance approval rates and loan performance.

More Use Cases

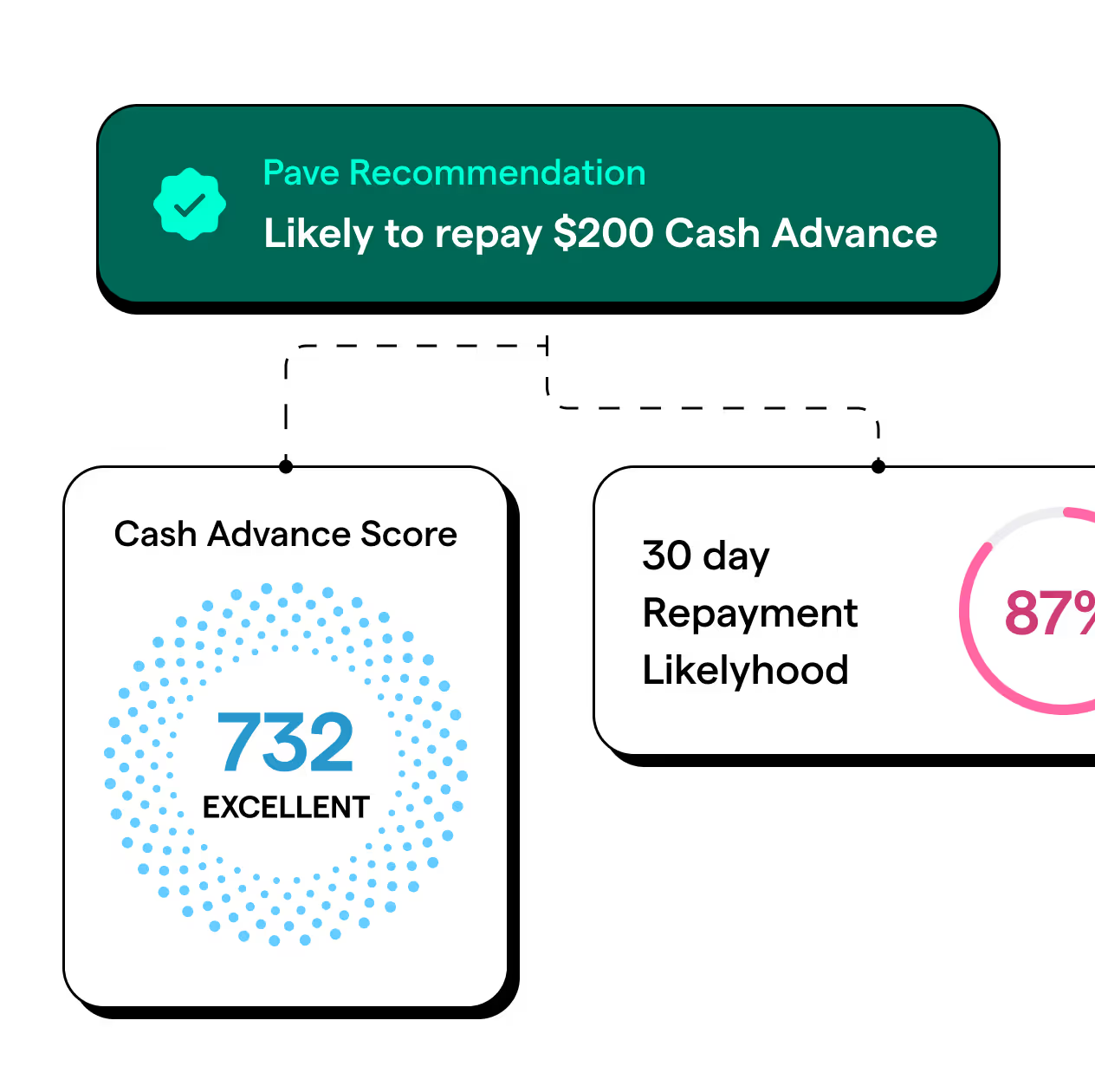

Cash Advance

Score users to increase approvals, advance amounts, and improve repayments.

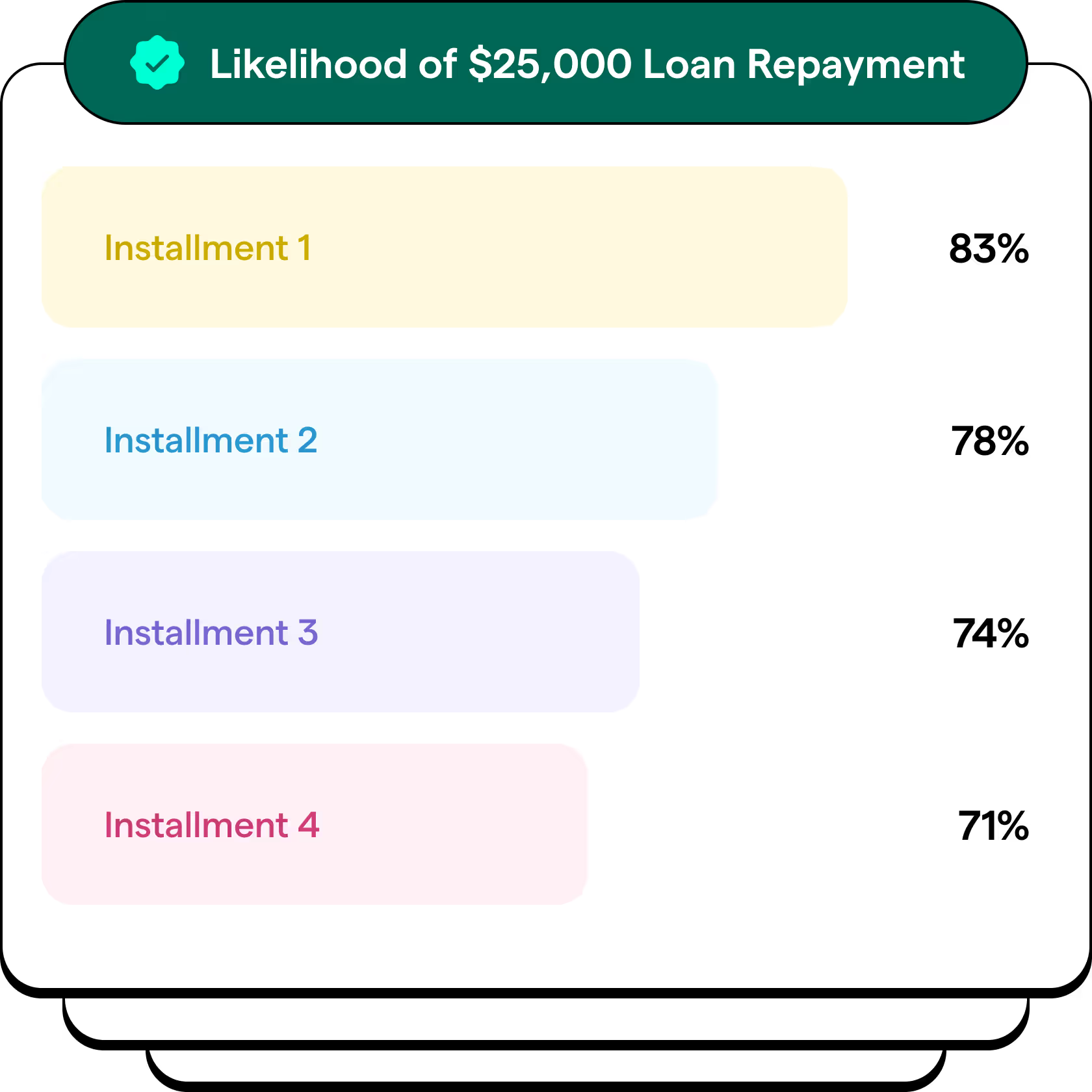

Small Dollar Loans

Predict repayment likelihood for the first 4 payments to reduce defaults.

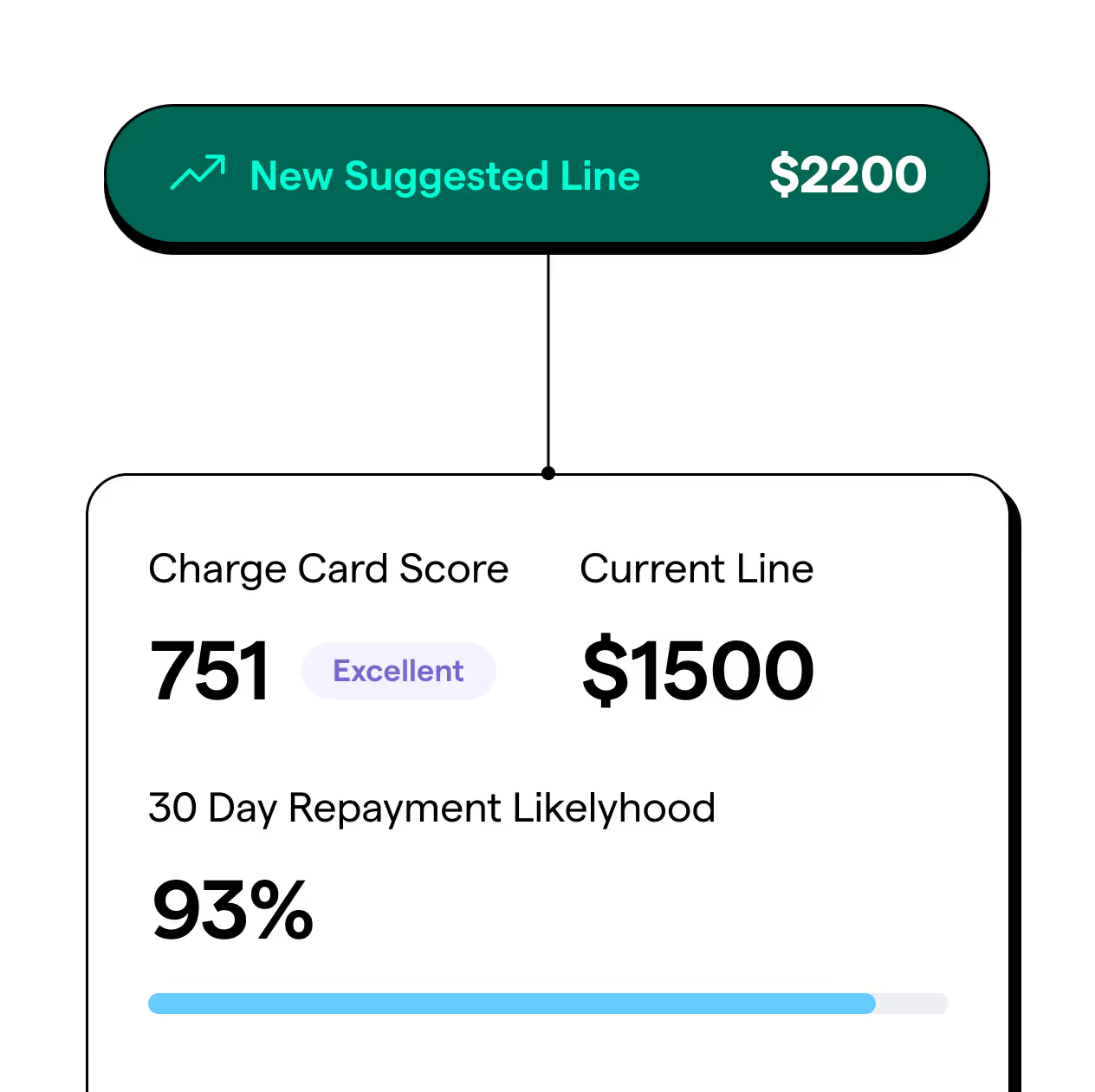

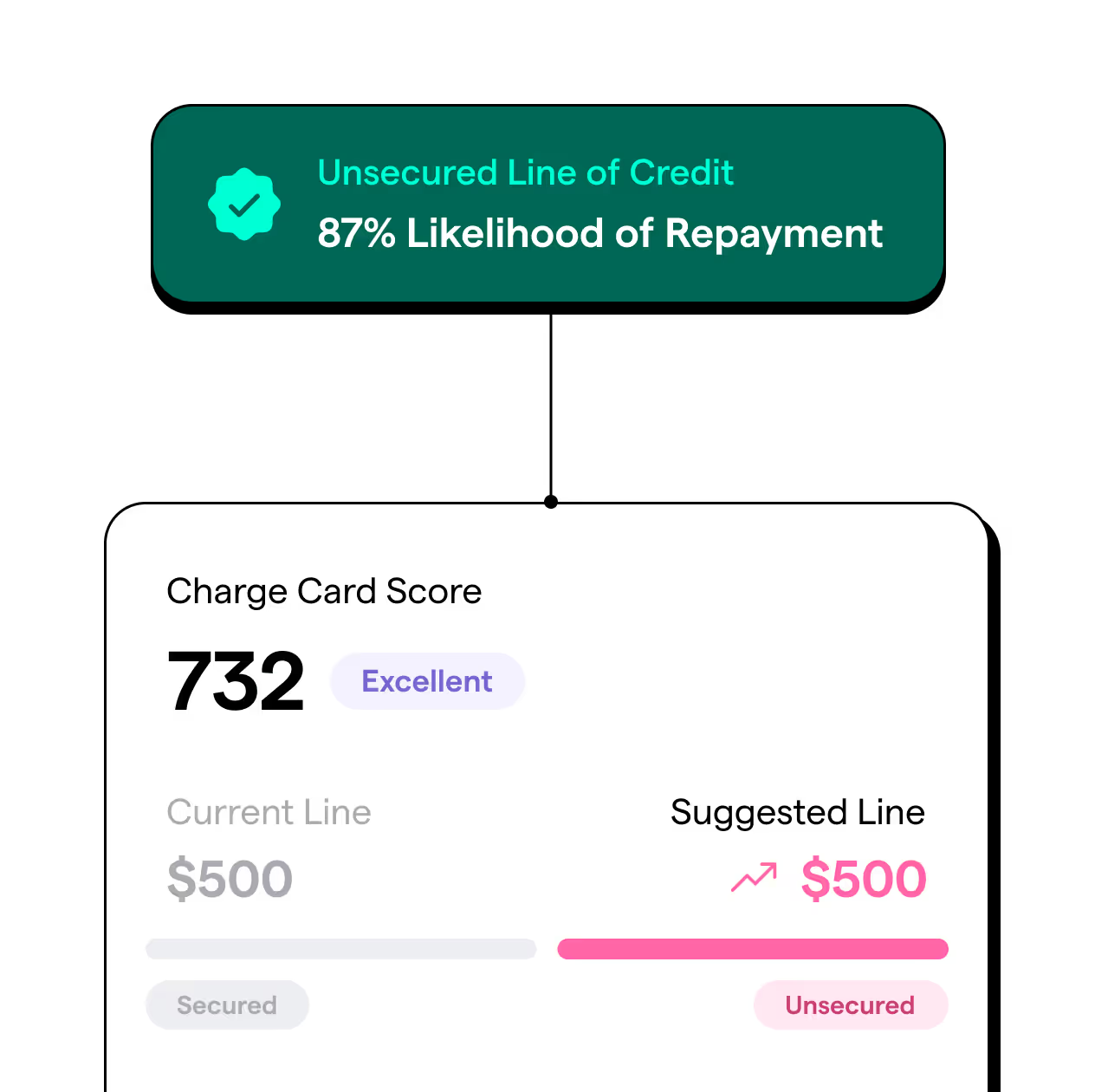

Charge Cards

Graduate users to higher secured or unsecured limits based on increased affordability.

Credit Cards

Set dynamic credit limits based on users' income and affordability.