Credit card defaults increased every month from December 2021 through April 2022. On top of that, it can take up to 60 days after a payment’s due date for a lender to report a missed payment. Lastly, Buy Now, Pay Later usage increased 115% year-over-year for first-time users.

These trends mean lenders need to get a real-time view into how a borrower’s financial situation is changing to reduce exposure to delinquencies and defaults.

BNPL in particular is changing how people borrow and spend. However, BNPL payments typically don’t get reported to the credit bureaus. It’s been hard for lenders to see a comprehensive and real-time picture of a consumer’s income, debt payment, and spending behavior – Pave.dev’s Cashflow Insights are changing that.

As new credit products like BNPL emerge, consumer lenders need to understand a real-time view of a borrower’s affordability.

In this post, we’ll discuss:

- How BNPL can affect a consumer’s credit default risk

- Pave’s data analysis on the rise of BNPL

- Challenges lenders face in gaining a real-time view of a borrower’s credit risk

- Drivers behind the growth of BNPL

Consumers are accumulating more debt via BNPL but FICO is unchanged

Picture this: A consumer has a FICO score of 700. They make purchases using BNPL, alongside some of their other loan payments in December. Over the course of the month, this individual gradually takes on additional debt in installments that amount to a larger sum by the end of the payment cycle.

Three things are notably happening here:

- Debt is increasing

- Disposable income is decreasing

- Credit score is not changing

BNPL purchases can add up to a significant sum owed across multiple platforms – even a bunch of small transactions can quickly and significantly lower an individual’s ability to finance other debt. Reports show that consumers (particularly Gen Z) are racking up debt. Bloomberg highlights how one borrower accumulated $5,000 in debt across three BNPL companies in just two months – none of this is showing up in a credit report!

On the flip side, imagine a thinly-filed consumer with a limited credit history. They use BNPL to help them afford essential purchases and make timely payments. They’re demonstrating positive credit usage behavior! This information is also not represented in credit reports. Lenders should be able to consider this behavior when deciding whether or not to extend credit.

Many BNPL providers are currently not furnishing data to the bureaus. It’s the same story with utility payments. Bureaus hold a wealth of data, but the traditional FICO score struggles to incorporate and act upon this information.

There’s an entire lack of visibility into BNPL. In just a few weeks, a consumer can significantly impact their ability to finance other debt, and lenders don’t see this change in credit reports for months, if at all.

FICO is backward-looking and makes the assumption that historical behavior is highly predictive of future performance. As new credit products emerge and loan defaults and delinquencies rise, analyzing the consumer’s borrowing behavior beyond credit reports will be inevitable for every consumer lender.

A look into the data

We analyzed a sample dataset of 358,773 users who have made BNPL payments. These users represented over 9 million loan payments, of which 3 million were BNPL payments.

Here are some interesting findings:

Top BNPL Companies by payment volume

The most popular BNPL companies in our sample dataset by payment volume were Afterpay, Klarna, and Zip.

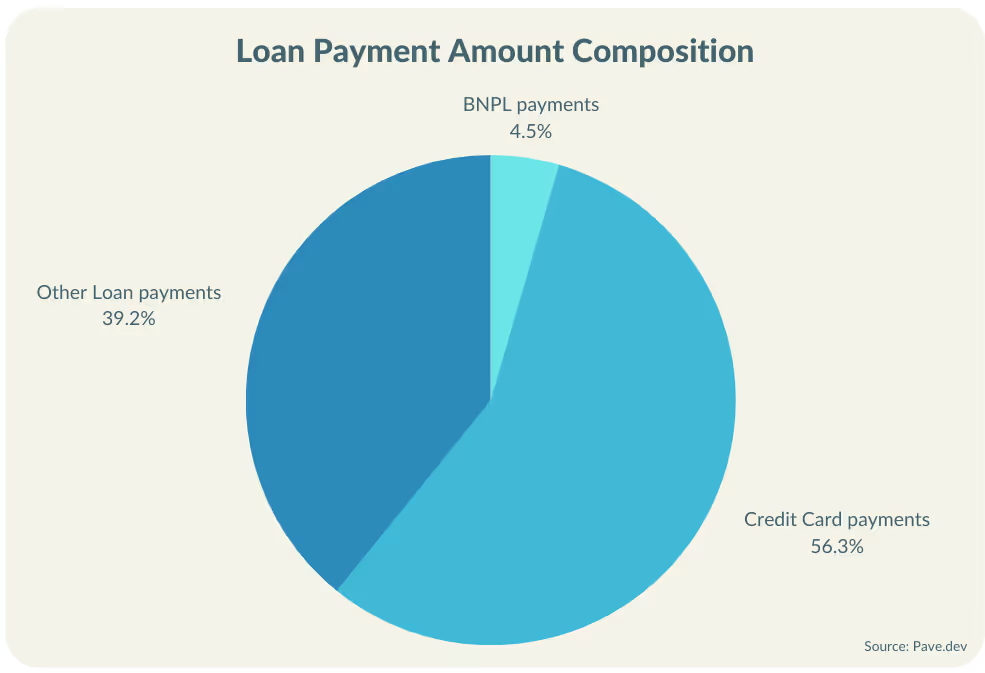

BNPL Payments now account for 4.5% of Total Loan Payment Amounts

Looking at the users in our sample dataset that have used BNPL, we found that 4.5% of their total loan payment amounts were BNPL payments. Our sample dataset represented $2 billion worth of loan payments across 9 million borrowers. Of this, BNPL payments made up $100 million across 3 million borrowers.

Credit cards made up 56.31% of loan payment amounts. Other loans, including student, auto, and lease-to-own made up 39.18%.

The percentage of BNPL payments in an individual’s loan profile is subject to further growth in the next few years. In 2021, the BNPL market was valued at $141.8 billion. Over the 2021-2026 period, it’s expected to grow at a CAGR of 33.3%.

According to reports on consumer spending, credit card spending has decreased, while the use of BNPL has increased as an alternative. 44% of US credit card holders report that they’d consider alternate financing options like BNPL to credit cards when making larger purchases, due to more attractive interest rates and fees compared to credit cards.

Overall, a growing population is using BNPL, the amount people are borrowing is increasing, and more borrowers are getting approved for BNPL loans.

The CFPB reported that the average BNPL loan amount was $121 in 2019 and grew to $135 in 2021. BNPL loan approval rates are also rising – companies approved 73% of applicants in 2021, compared to 69% in 2020.

BNPL is gradually changing the lending environment, as more people use BNPL to finance their needs and lifestyles.

BNPL Data Creates the Opportunity for Granular Decision-making

Given this growth, lenders should consider a consumer’s real-time cashflows and fluctuations in their ability to pay. BNPL usage can signal both negative and positive spending and repayment behavior. Either way, this context is being excluded from credit reports.

Real-time insight into the consumer’s borrowing behavior and cashflows allows lenders to:

- Continually monitor and adjust credit limits

- Refine loan approval amounts

- Make precise underwriting decisions

- Optimize interest rates

- Maximize collections success

Overall, the flexibility of BNPL significantly impacts how much additional debt a person can afford. Lenders who aren’t looking at the borrower’s cashflow risk offering debt to individuals who may not be able to meet their payments.

Challenges Lenders Face with the Growth of BNPL

BNPL growth presents several challenges for consumer lenders:

Increase in BNPL usage is complicating a borrower’s credit profile

38% of buy now, pay later borrowers use BNPL once a month or more. 67% of buy now, pay later borrowers think BNPL could replace their credit cards. As more alternatives to traditional credit emerge in the consumer market, a given individual’s financial profile is becoming increasingly complex.

Increase in BNPL Delinquencies is affecting borrower credit risk

Numbers from Affirm point to increasing delinquencies from 1.5% in 2021 to 2.7% in the same quarter in 2022. 33% of BNPL users have made a late payment or incurred a late fee in 2022. Increasing BNPL delinquencies show that borrowers are becoming riskier in this spending category, which affects their overall risk.

Lack of BNPL usage data in credit reports gives an incomplete view of consumer liabilities

Lenders heavily rely on credit reports to understand their customers’ financial history. Still, companies largely aren’t reporting BNPL usage information to the bureaus. As a result, this skews FICO scores and credit reports. Without BNPL data, lenders depend on an incomplete image of their customers.

Alongside these challenges, profit margins for lenders are decreasing – in 2021, margins were 1.01% of the total amount of loans originated, compared to 1.27% in 2020. To account for rising defaults, lenders need to be more critical in credit decisions – including considering a more real-time view of a borrower’s cashflows and liabilities – to lower their losses.

Key Drivers behind the Growth of BNPL

A consumer’s financial profile is becoming increasingly complicated with the onset of many financial products, including BNPL. Below are some key drivers behind BNPL and why it’s likely here to stay.

Rising cost of essential goods

Millions of people continue to live paycheck to paycheck due to the rising cost of essential goods like gas and groceries. As people struggle to pay their bills and emergency expenses, many turn to the flexible payment options that BNPL provides. In September 2022, Zip reported a 95% increase in BNPL usage for grocery items. Klarna reported that more than 50% of their user purchases are household or grocery items.

Rise of BNPL for everything from vet bills to weddings

More BNPL companies are joining the landscape, and the BNPL market is estimated to reach $3.98 trillion by 2030. People now use BNPL to spend across many categories beyond retail, including rent (Jetty), healthcare (Walnut), dental and vision (Cherry), weddings (Carats & Cake), vet bills (GoFetch), and even gas stations like Chevron are accepting BNPL.

Lack of credit access

57 million Americans live with subprime credit, and 1 in 3 American adults aren’t able to obtain a credit score. They’re often denied financial services like credit cards and loans and pay higher interest rates for the credit products they access. On top of that, over 70% of BNPL users are Millennials or Gen Z, who also have limited financial flexibility and less financial experience. Millennials cite a lack of access to credit and less credit history as the reason they turn to credit-free financing options. Consumers can use BNPL even if their credit score is not in good standing.

Impulse purchasing

Although BNPL can be a tool that makes purchases more accessible, it can encourage impulsive purchasing. For non-essential BNPL purchases like clothing, psychological factors like the pain of paying in full can influence consumers. Buy Now, Pay Later provides instant gratification and affordability to consumers, causing 55% of BNPL customers to spend more than they would with other payment methods.

Bottom Line

The lending environment is becoming increasingly complex. The lender’s path to reducing risk while lending to as many people as possible is also more complicated. As new credit products like BNPL emerge, Cashflow Underwriting will be inevitable for every consumer lender.

Adding alternative credit data is not as easy as adding it to the existing system – there needs to be an entirely new structure for the consumer financial profile. Credit scores are backward-looking, evaluating borrowers today on past behavior. Alternatively, Cashflow Insights give a real-time view into changes in a person’s finances and predictions for the future.

How Pave Empowers Lenders with Cashflow Insights

Pave makes it easier to build cashflow-based underwriting models that account for alternative credit data like BNPL usage. This allows lenders to comprehensively view a user’s income, liabilities, and expenditures.

Pave offers a few products to help companies build out their approval process, minimize defaults, and improve customer financial health:

- 300+ Risk and Affordability Attributes to analyze a user’s balance history, loan payments (including other BNPL), cash advance history, recurring expenses, spending patterns, fees, income history, and more.

- Likelihood to Repay Score that predicts the likelihood a user will repay a cash advance or loan within a given period of time. Our score is trained on a growing dataset of millions of cash advance deposits and repayments, allowing newer fintechs to take advantage of a large training dataset that they’ve not yet accumulated.

- Our Payroll Prediction Model allows companies to forecast when to pull a loan repayment, reducing the risk of pulling the repayment too early and causing the user to go into overdraft.

Alternative credit data enables lenders to differentiate and stand out in the market. Build, launch, and scale risk models based on granular details into a user’s entire cashflow, not just what bureaus traditionally report.

See how our Cashflow API powers insights for Tracking bills including BNPL.

Interested in learning more? Let us know.