How Pave’s Fuel Charge Card Score Helps Providers Approve New Businesses with Confidence

Fuel card providers play a vital role in enabling businesses in the fleet and trucking industry to manage one of their most critical operational expenses—fuel. However, traditional credit models often fall short when assessing repayment risks, especially for small businesses with limited credit histories seeking access to credit. Rising delinquencies further complicate underwriting, leaving providers cautious about extending credit and eager for better tools to mitigate risk without slowing growth.

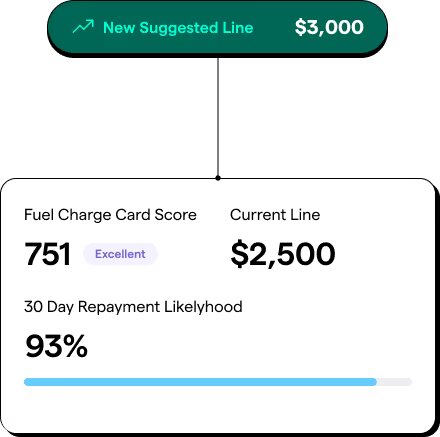

Pave’s Fuel Charge Card Score addresses these challenges head-on. By leveraging real-time cashflow data, and Pave’s proprietary Cashflow Attributes—such as revenue trends, expense stability, and recurring payment behaviors—this predictive score, tailored to fuel expenses, empowers fuel card providers to assess financial health with greater visibility and precision. Providers can:

- Confidently approve more businesses

- Reduce delinquencies

- Expand into new industries like logistics and construction

Check out this video:

How Pave’s Fuel Charge Card Score Changes the Game

Traditional credit scores attempt to broadly rank-order businesses, but they often overlook the unique financial behaviors tied to specific products like fuel charge cards. Repayment risk hinges on factors deeply rooted in the industry. For example, fleet companies often have cyclical cashflows influenced by fuel price fluctuations, maintenance schedules, and contract payments. These time-sensitive financial patterns are critical to understanding repayment risk—nuances that traditional models frequently overlook.

At Pave, we’ve designed the Fuel Charge Card Score to change the game for fuel card providers. It’s purpose-built to predict whether a business will repay its fuel charge card balance within 30 days. Here’s how it works:

- Real-Time Financial Data: We analyze up-to-date revenue, expense patterns, and account balances to provide an accurate, current view of a business’s financial health.

- Fuel-Specific Insights: Our models incorporate transaction data and recurring patterns tied directly to fuel-related expenses, offering tailored predictions.

- Unified with Traditional Credit Data (if available): Complementing cashflow insights with credit reports ensures a comprehensive assessment.

At Pave, we don’t just build scores; we build insights grounded in robust, diverse datasets specific to fleets, including fuel repayment risk.

By unifying diverse, fuel-specific datasets, the Fuel Charge Card Score offers a nuanced, actionable view of a business’s financial behavior and repayment capacity.

Together, these data sources create a nuanced view of a business’s financial behavior and repayment capacity.

Reducing delinquencies by 68% while maintaining approvals

For one Fuel Charge Card provider, the impact was transformative.

Leveraging the Fuel Charge Card Score, the provider reduced their 15-day delinquency rate by 68.49% and their 5-day delinquency rate by 53.05%.

[Insert chart showing approval and delinquency trends before and after implementation]

How did we achieve this? By analyzing:

- Revenue Stability: Businesses with steady revenue streams, even if seasonal or fluctuating, were identified as lower risk.

- Savings and Liquidity: High cash reserves or consistent end-of-month balances strongly predicted repayment reliability.

- Repayment Trends: Businesses with a proven history of meeting smaller obligations, like small-dollar loans, demonstrated capacity for timely repayment of larger balances.

With these insights, fuel card providers can confidently say "yes" to more businesses, including those in underserved segments, while minimizing risk and supporting sustainable growth.

Why Pave Is Different

What makes Pave’s scores stand out for fuel charge card providers? It starts with the data. Our scores are trained on diverse datasets from around 20 million anonymized unique users, including both consumers and businesses. This enables us to move beyond broad generalizations, offering tailored insights to meet the specific needs of fuel charge card providers.

Our models stay ahead of the curve by regularly retraining to adapt to market shifts and evolving borrower behaviors. This agility helps providers navigate economic uncertainty with confidence.

The Fuel Charge Card Score focuses on repayment behaviors specific to fuel charge cards. Instead of relying on generic credit signals, it pinpoints real-time financial patterns—like steady revenue streams, consistent cash reserves, and fuel-specific spending patterns—to predict whether a business will pay its balance within 30 days.

For instance, a small fleet with irregular revenue might be flagged as risky by generic models. The Fuel Charge Card Score digs deeper, identifying reliable repayment indicators that traditional credit scores overlook.

This product-specific approach enables fuel card providers to:

- Approve More Businesses: By analyzing cashflow patterns tied to fuel repayment, providers can confidently extend credit to businesses often overlooked by generic scores.

- Expand Inclusivity: Small businesses, gig-economy fleet operators, and startups with unconventional cashflow patterns gain fair access to credit.

- Manage Risk Effectively: Approving more businesses doesn’t mean taking on more risk. Tailored insights ensure a balance between growth and portfolio health.

With the Fuel Charge Card Score, inclusivity in lending isn’t just possible—it’s practical. Make smarter decisions and help more businesses access the fuel credit they need to grow.

Real-World Impact: Businesses and Providers Win Together

What does this mean in practice? Let’s break it down.

For Businesses:

- A new logistics company with limited credit history gets approved for a fuel card, keeping operations running smoothly.

- A seasonal business with inconsistent revenue secures a higher credit limit, aligned with their peak earnings periods.

For Fuel Card Providers:

- Delinquencies drop—by 68.49% for 15-day delinquencies and 53.05% for 5-day delinquencies.

- Portfolios grow sustainably, balancing profitability with inclusivity.

The result is a win-win. Businesses get the fuel credit they need to thrive, and providers grow their customer base while maintaining portfolio health.

Fueling Smarter Decisions

The fuel card industry is evolving, and success belongs to providers who move beyond generic risk assessments. With Pave’s Fuel Charge Card Score and Cashflow Attributes, you won’t just approve more businesses—you’ll approve the right businesses.

Ready to transform your fuel card offering? Let’s connect to explore how the Fuel Charge Card Score can help your business approve more applicants, reduce risk, and unlock new growth opportunities.