A Quick Overview:

Let’s recap the key points from Part 1 of this blog post:

- Recent trend: Higher-income individuals are increasingly using alternative credit products

- Half of Americans – including people earning over $100,000 – face liquidity constraints

- Score inflation and risk uncertainty are causing banks to pull back on consumer loans

- These trends are fueling consumer demand for increased access to credit

In this post, we’ll look at how lenders are using cashflow data to increase financial access for underserved borrowers and gain a competitive edge.

Traditional scoring alone is insufficient for credit risk assessment

Even high-earners face loan denials

In our recent data study, we found that a new segment of individuals face denials from traditional lenders: high-income borrowers.

The median income of alternative credit users increased 30% in 6 months, meaning more high-income individuals are increasingly using alternative credit products as they face denials from traditional lenders.

The underserved market is growing – it’s no longer who we’ve commonly thought it to be, which was often subprime, thin-filed, and low-income individuals.

In Alex Johnson’s recent essay, he cites the LendingClub and PYMNTS report that details how living paycheck-to-paycheck is not just a reality for low-income consumers – now it includes almost 50% of people earning $100,000 a year.

Why is this overall market expanding?

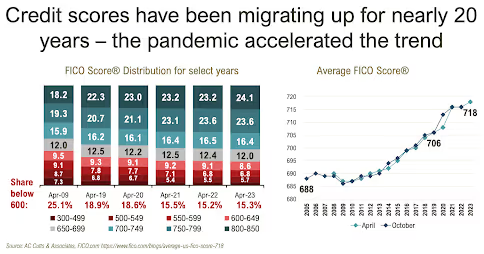

Credit scores continue to inflate each year

Over the past two decades, credit scores have consistently trended upward, accelerated by the pandemic.

This can create a mismatch between a borrower’s current affordability and creditworthiness assessment, impacting access to favorable credit terms even for high-earning individuals.

Credit scores and reports don’t quickly adjust to changes in affordability

Credit reports often lag in reflecting real-time financial changes taking up to 60 days to record events like missed payments or debt repayments. Whether it’s changes in delinquency status, or upward trends in debt payoff, traditional credit scores often don’t promptly reflect these changes.

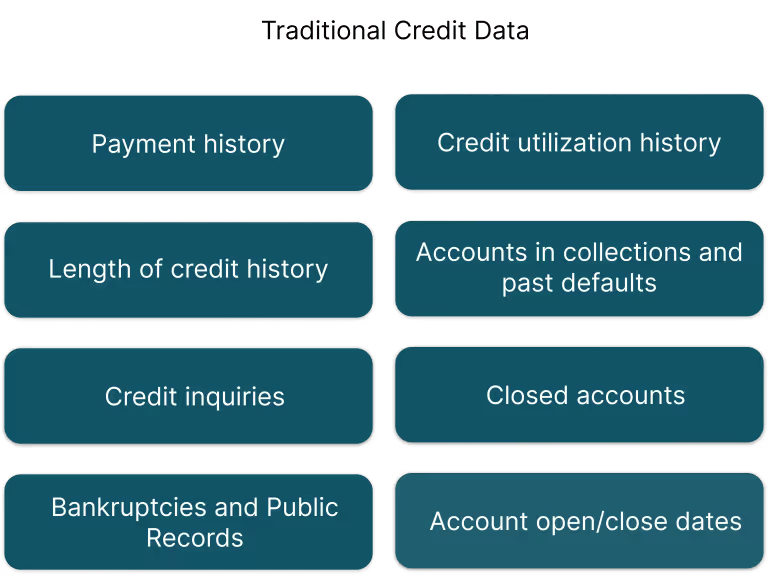

Primarily backward-looking, these reports focus on past financial behaviors to assess creditworthiness, providing a limited view of current financial well-being.

Here are the types of data credit reports return, which are largely backward-looking:

While credit reports are useful for understanding an individual’s historical financial behavior, they don’t provide a comprehensive or real-time picture of their financial health or risk. High-earners, despite their substantial income, may encounter increased loan denials due to the lack of visibility into current affordability.

The Rise of Cashflow-Based Risk Assessment

A new market of credit is emerging

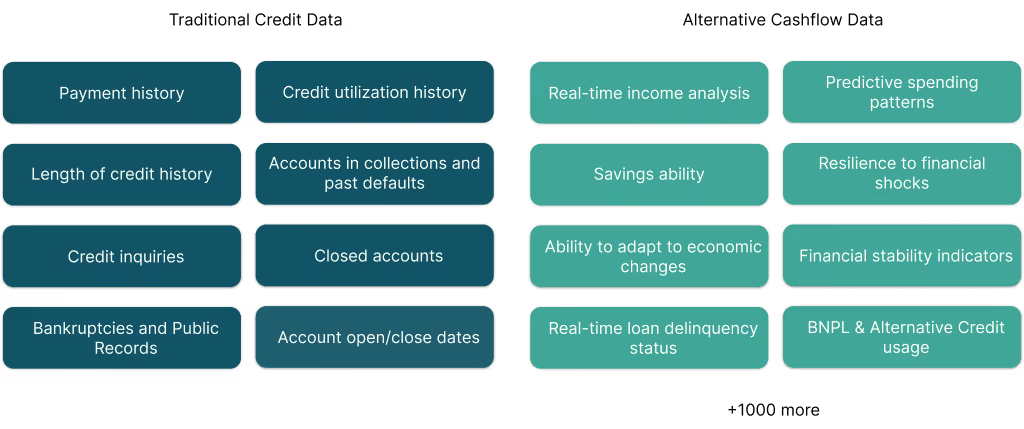

Living paycheck-to-paycheck is a widespread financial challenge affecting individuals across income brackets. Innovative lenders and fintechs use cashflow data, alongside traditional credit information, to gain a competitive edge in an evolving market.

People are already seeking alternatives to traditional credit:

What cashflow data tells us about current and projected affordability

Cashflow data provides a real-time and comprehensive view of an individual’s current and future affordability such as:

- If they have a regular income

- Whether they’re paying bills and liabilities on time

- Account balance trends

- Overdrafts and NSF history, and more.

By incorporating this data alongside credit reports, lenders make more informed risk decisions based on a more comprehensive view of affordability.

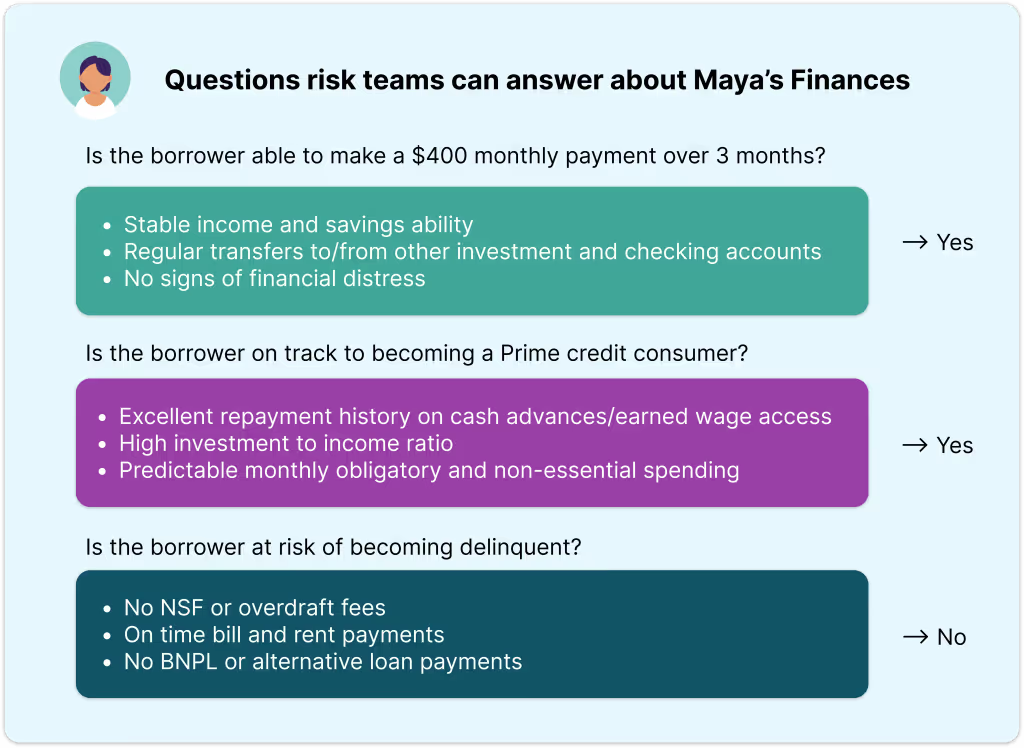

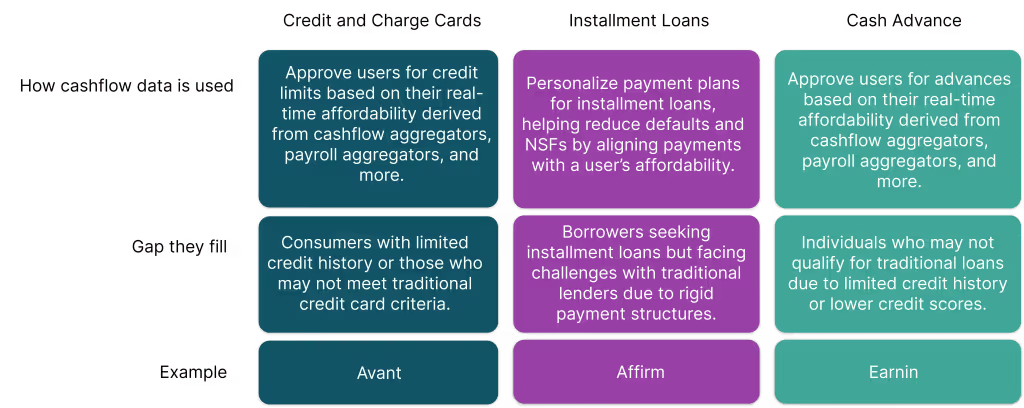

Lenders use cashflow analytics to expand who gets access to credit and what products are available

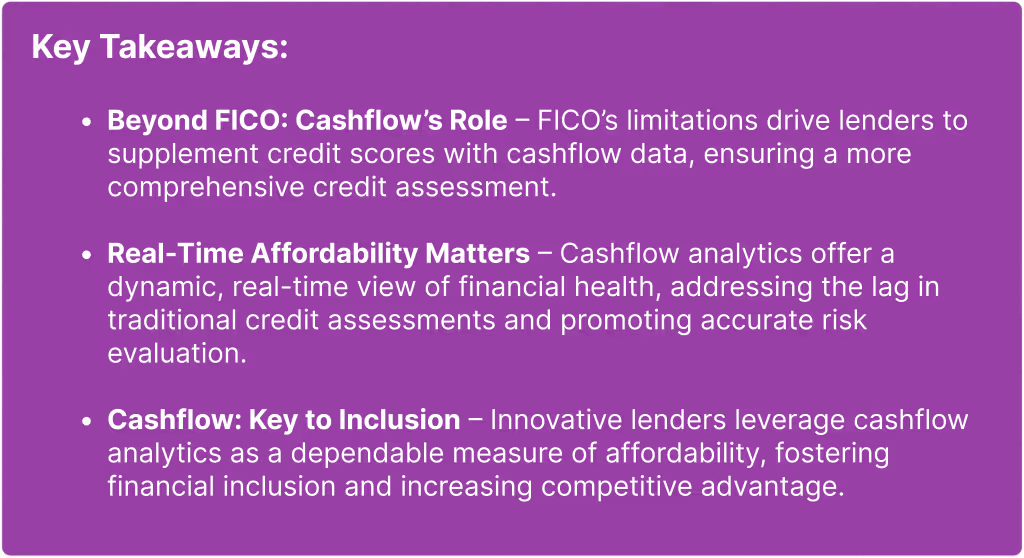

Lenders use cashflow data to get a more accurate depiction of current affordability, which allows them to address the limitations of traditional scoring and position themselves as industry leaders.

Real-time analysis of income, bill payments, and account trends enables previously rejected individuals to showcase financial responsibility, challenging the assumption that lower credit scores imply an inability to repay.

Lenders use cashflow data in the following ways:

Cashflow analytics prove to be a reliable measure of affordability

Cashflow helps lenders pinpoint creditworthy borrowers often overlooked by traditional scores

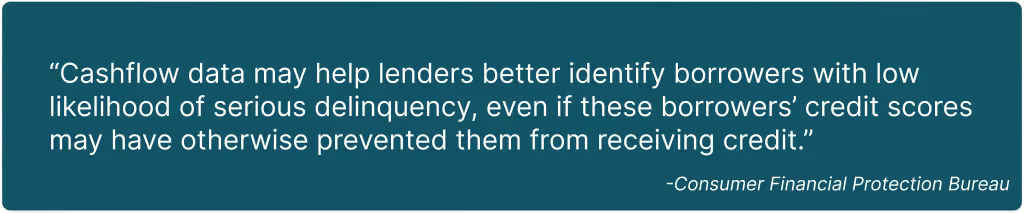

A recent CFPB report confirms the reliability of cashflow analytics, showing individuals with positive cashflow (high savings, regular savings, no overdrafts, no trouble paying bills) outperform similar credit score groups by 20% in loan repayment.

Additional studies reveal a strong correlation between bill payment history and future mortgage payments, emphasizing the potential to use these payment behaviors as additional signals in the underwriting process.

A study from the FinRegLab analyzed data from six non-bank financial service providers to examine the effectiveness of cash-flow variables and scores in credit underwriting, especially for consumers and small businesses traditionally underserved by conventional credit systems.

They found the following on cashflow analytics:

- Predictiveness: Cash-flow variables and scores demonstrated a robust ability to predict likelihood of default, with AUCs ranging from 0.592 to 0.725 across diverse populations and products.

- Combination with Traditional Data: Cashflow data, when combined with traditional credit assessments, improves risk prediction. It uniquely identifies risk levels among borrowers who might appear similarly risky under traditional scoring systems.

- Inclusiveness: The study indicated that cash-flow data broadens access to credit, especially with borrowers who have low or no traditional credit scores.

- Fair Lending Effects: Cash-flow data reliably predicted credit risk across different demographic groups, as indicated by consistent AUC values, without disproportionately affecting protected populations.

The research suggests that cash-flow data, alone or in conjunction with traditional data, holds promise for enhancing credit risk prediction and expanding credit access, warranting further investment in research and technology.

Future innovation in cashflow analytics

The user profile for credit is changing – 50% of Americans with substantial incomes still live paycheck to paycheck.

Incorporating cashflow analytics allows lenders to make more informed decisions, broadening credit access and securing a competitive edge. This provides a more inclusive credit evaluation, aligning credit scores more closely with actual financial health and providing individuals with essential resources to manage financial hurdles.

Check out our use cases for: