How Pave’s Flexible Rent Scores Help Property Management Solutions Providers Approve More Tenants with Confidence

.avif)

The Approval Dilemma: Growth vs. Risk

Every property management provider faces a tough choice: approve more tenants and risk defaults, or play it safe and miss out on great renters. Traditional credit scores like FICO don’t make it easier—they’re outdated, overly broad, and ignore the nuances of today’s renters.

But here’s the thing: the risk of paying rent is fundamentally different from the risk of paying a credit card. Rent is tied to shelter—a borrower’s most basic need. That difference demands a score that reflects the unique urgency of rent payments.

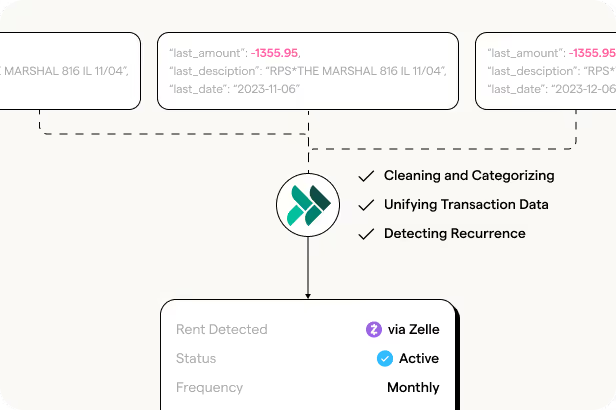

Enter Pave’s Flexible Rent Score. Purpose-built to predict whether a tenant will make their payment within a given month, it leverages real-time banking data and a tailored dataset specific to rent installment loans, allowing providers to confidently expand approvals without increasing risk.

Check out this video:

How Pave's Flexible Rent Score Changes the Game

Generic credit scores aim to rank-order tenants broadly but don’t consider the unique repayment behaviors tied to specific products like flexible rent installments. A score tailored to rent repayment risk must reflect the time sensitivity around housing—and the real-time financial factors that predict whether a tenant will pay on time.

At Pave, we’ve designed our Flexible Rent Score to do just that. It’s purpose-built to predict whether a tenant will make their payment within a given month. Here’s how it works:

- Real-Time Bank Transactions: We analyze current income, spending, and balances for the most up-to-date view of financial health.

- Performance Data from Flexible Rent Products: Our models are trained on repayment patterns specific to rent, ensuring precise predictions.

- Unified with Credit Reports (if available): We incorporate traditional credit data to complement our cashflow-based insights.

At Pave, we don’t just build scores; we build insights grounded in robust, diverse datasets specific to rent repayment risk.

Together, these data sources create a nuanced view of a borrower’s financial behavior and repayment capacity.

Doubling Approvals while Reducing Risk

For one flexible rent provider, the impact was transformative.

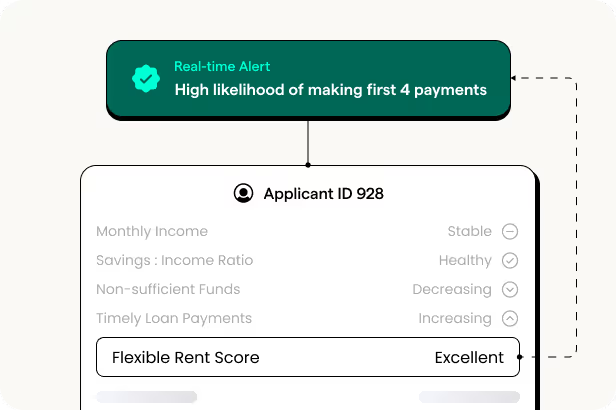

Leveraging the Flexible Rent Score, the provider approved all users with at least a 90% chance (0.904) of paying their rent installment within a given month.

- Approvals jumped from 18% to 50%.

- Collections dropped from over 30% to under 6%.

How did we do it? By analyzing:

- Income Stability: Tenants with a strong history of income, even if irregular, proved to be lower risk.

- Savings Behavior: High balances in primary accounts post-payroll strongly predicted repayment reliability.

- Repayment Trends: Tenants who consistently repay smaller obligations, like cash advances, showed they could handle larger loans.

With these insights, providers can confidently say “yes” to more tenants, even in nontraditional segments.

Why Pave Is Different

What makes Pave’s scores stand out? It starts with the data. Our scores are trained on diverse datasets of around 20 million anonymized unique users, covering both traditional and nontraditional (subprime and near-prime) borrowers. This means we don’t just generalize risk — we pinpoint it, tailoring insights to fit the specific needs of each lender.

Our models stay ahead of the curve by adapting to changing markets, retraining regularly to reflect current tenant behaviors. This agility helps property managers navigate economic shifts with confidence.

Pave's Flexible Rent Score focuses on time-sensitive repayment behaviors specific to rent. Instead of relying on broad risk categories, it pinpoints real-time financial patterns — like consistent payroll deposits or healthy post-payroll balances — to predict whether a tenant will pay rent within a given month.

For instance, a gig worker with irregular income might be flagged as risky by generic scores. Pave’s Flexible Rent Score digs deeper, identifying reliable repayment indicators that generic models miss.

This product-specific approach helps property management solution providers:

- Approve More Renters: By pinpointing behaviors tied to rent repayment, you can confidently say “yes” to more tenants who might be overlooked by generic scores.

- Expand Inclusivity: Gig workers, part-time employees, and retirees—whose financial patterns don’t fit neatly into broad risk categories—get the chance they deserve.

- Manage Risk Effectively: Approving more tenants doesn’t mean taking on more risk. Insights tailored to rent repayment help balance growth and portfolio health.

With Pave’s Flexible Rent Score, inclusivity in lending isn’t just possible—it’s practical. Make smarter decisions, and get more renters access to the housing they need. It’s a win-win that generic scores can’t achieve.

Real-World Impact: Tenants and Property Managers Win Together

What does this all mean in practice? Let’s break it down.

For Tenants:

- A renter with little credit history finally gets approved for a flexible rent installment loan.

- A part-time gig worker, overlooked by traditional models, secures financing their security deposit.

For Property Managers:

- Approval rates soar—from 18% to 50% in the case of one flexible rent provider.

- Defaults drop from 30% to under 6%.

- Portfolios grow with confidence, profitability, and impact.

The result is a win-win. Tenants get access to the housing and credit they need, and lenders expand their market while maintaining healthy portfolios.

The Future of Flexible Rent is here

The property management landscape is evolving, and success belongs to providers who move beyond generic risk assessments. With Pave’s Flexible Rent Score and cashflow attributes, you won’t just approve more tenants—you’ll approve the right tenants.

Ready to transform your property management or flexible rent solution? Let’s connect and build a future where more renters get the housing they need, and your approvals are smarter, safer, and more profitable.