As new credit risk scores emerge, there’s a growing promise of better insights and predictive power, especially through the use of real-time bank transaction data. However, navigating these new scores—particularly cashflow scores—can be confusing. Understanding how these scores work and assessing their real-world impact is crucial.

We’ll address:

- The limitations of traditional scores like FICO

- How cashflow scores address these gaps

- How cashflow score(s) should ideally be designed

FICO: What It Is and What It Isn’t

FICO has been the backbone of credit scoring for decades, providing lenders with a standardized way to assess borrower risk. It has been essential for securitization and remains a trusted tool across financial institutions.

FICO is a rank-ordering score, which means it ranks borrowers by comparing their likelihood of default relative to others. For example, a borrower with a FICO score of 750 is considered less risky than one with a score of 600. This rank ordering is valuable for broad risk segmentation and general decision-making across a wide variety of loan products.

However, the emergence of new credit products like Buy Now, Pay Later (BNPL), small dollar loans, and other fintech innovations has created a shift. These products serve a new era of borrowers— those underserved by traditional credit products. As lending becomes more complex with new products and borrowers, lenders need more tailored insights into borrower behavior. For instance, a borrower who frequently uses BNPL has a very different risk profile than someone taking out a $50k personal loan.

While FICO’s rank ordering excels at giving a broad view of risk, it doesn’t provide the detailed, real-time predictions lenders increasingly need to manage specific loan types more effectively.

For example, FICO scores can’t tell lenders:

- How likely a borrower is to make their next few payments

- Whether a borrower is better suited for a credit card but might struggle with an installment loan

FICO’s broad applicability is its strength, but for lenders focused on specific loan types or near-term risk, more precise, product-specific tools are required to make actionable decisions.

How Cashflow Scores Address FICO's Gaps

Cashflow scores, built on real-time transaction data, address many of the limitations of traditional credit scores. FICO, while foundational in lending, doesn’t provide the real-time insights lenders need in today’s fast-paced environment. Cashflow scores address this by tracking daily financial behaviors such as income streams, spending patterns, and payment history. This allows lenders to assess a borrower’s current financial situation and make more informed, near-term predictions like:

- The likelihood of a borrower making their next few payments.

- Early signals of financial stress, such as missed payments or irregular income

This allows lenders to intervene before delinquency. While FICO provides a generalized view of creditworthiness, it doesn’t adapt quickly to changes in a borrower’s financial behavior. Cashflow scores fill that gap by delivering real-time visibility into financial health, which traditional scores miss.

What Ideal Cashflow Scores Should Look Like

Not all cashflow scores are created equal. To realize their full potential, cashflow scores must be built with a deep understanding of the credit product they are evaluating, rather than a one-size-fits-all approach. The most effective cashflow scores should:

- Be product-specific: Cashflow scores should be trained on data specific to the type of credit product they are assessing (e.g., personal loans, credit cards, or BNPL) and the borrowers they serve. This way, cashflow scores can capture the unique risk of emerging borrower segments.

- Provide near-term predictions: Unlike generalized rank-ordering scores that take months to validate, cashflow scores should provide actionable insights within weeks, such as the likelihood a borrower will pay their first four payments – crucial for evaluating borrowers who may be new to credit.

- Deliver granular insights: These scores should offer detailed predictions, such as how likely a borrower is to make their next payment, rather than just placing borrowers into broad risk categories.This level of detail helps lenders better understand the unique financial behaviors of new borrower segments.

An ideal cashflow score is more than just a risk indicator—it’s a tool that enables lenders to predict repayment behavior based on dynamic, real-time financial data.

Why Product-Specific Scores Matter

Product-specific scores delve deeper into the nuances of repayment patterns, which can vary significantly across different loan types. For example, consider the differences between credit cards and buy now, pay later (BNPL) loans. Credit cards allow flexible payments, where a borrower might consistently make minimum payments without paying down their balance. In contrast, BNPL loans require fixed payments, and missing an early installment is a stronger signal of future default.

As more lenders expand into products like BNPL or small-dollar loans, they reach new borrower segments—many of whom have been underserved by traditional financial products. These borrowers often have financial behaviors that aren’t captured by broad risk scores like FICO, but are captured by cashflow scores, tailored to their borrowing habits and specific loan product to provide a more accurate, actionable risk assessment.

As the chart below shows, there’s a strong correlation between a borrower making the first four payments and the likelihood of full loan repayment. Borrowers who successfully make the first installment are significantly more likely to pay off their loan in full. This predictive power allows lenders to estimate the likelihood of loan payoff within weeks, rather than waiting for the entire loan term to unfold.

Why New Cashflow Scores Shouldn’t Mimic FICO’s Structure

Despite FICO’s proven success, new credit scores entering the market today – including generic “cashflow scores” should avoid replicating its structure due to:

- Limited Historical Data: Unlike FICO, which benefits from decades of diverse data, new cashflow scores lack this advantage.

- Unique Nuances: Generic rank-ordering scores are less equipped to handle the specific needs of niche products and borrower segments in today’s lending environments.

Consider this scenario:

A rank-ordering cashflow score built using data from a single credit card portfolio targeting middle-income borrowers may be effective for that group. However, it likely won’t generalize well to other products like BNPL, personal loans, or mortgages.

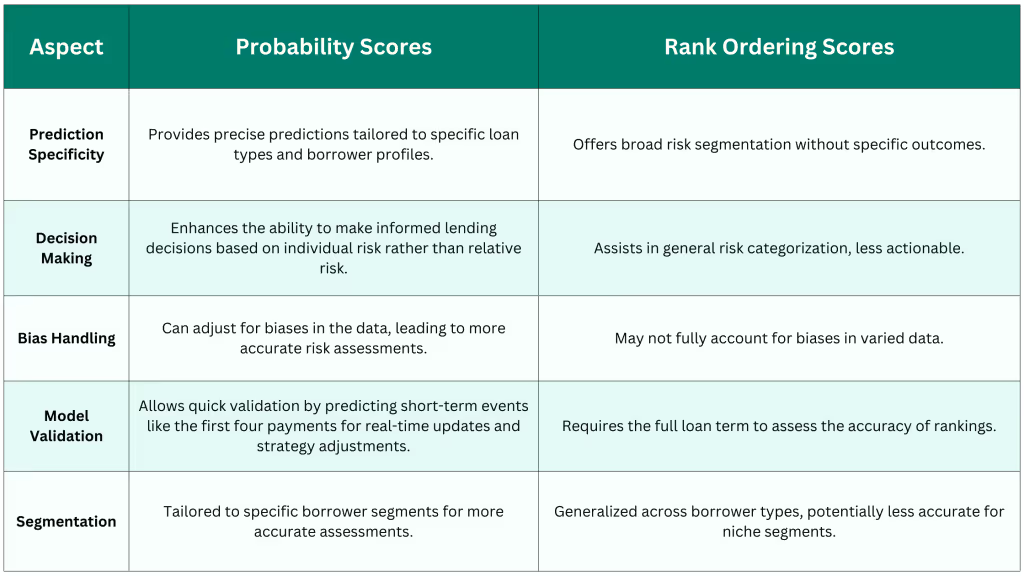

Here’s a breakdown of the issues associated with using a rank-ordering structure:

Product-Specific Probability Scores: A New Era in Lending

Product-specific probability scores are the next step in credit risk evaluation. These scores focus on predicting specific outcomes for different loan types. For instance, they can predict the likelihood that a borrower will make their 1st, 2nd, 3rd, and 4th payments for a short-term loan.

Unlike traditional rank-ordering scores, which group borrowers into broad risk categories, product-specific scores offer clearer distinctions between borrower profiles. This allows lenders to:

- Approve more low-risk borrowers without increasing portfolio risk

- Make more precise lending decisions based on a borrower’s actual financial behavior, not just their relative risk

By improving risk segmentation, product-specific scores allow lenders to confidently increase approval rates while maintaining or improving portfolio performance.

Conclusion

New credit scoring models should avoid following FICO’s method of ranking borrowers by relative risk and instead focus on providing specific repayment probabilities. Without the decades of diverse and comprehensive data that FICO has, new generic rank-ordering scores are likely to fall short of delivering accurate and fair assessments.

Adopting product-specific probability scores that utilize new datasets allows for more individualized and precise risk evaluations. This tailored approach offers a reliable assessment of borrower risk, leveraging detailed financial data without the need to replicate FICO’s extensive historical scope.

By embracing the power of product-specific probability scores, credit risk officers can lead their organizations into a new era of lending. This shift enables real-time decision-making, improved borrower insights, and enhanced portfolio performance, driving both innovation and competitive advantage.